One of the first decisions you'll make when starting a new business is choosing an entity type. Generally, most entrepreneurs choose to form a Corporation or a Limited Liability Company (LLC). Making the decision between LLC vs Corporation is an important step in the business formation process. The main difference between an LLC and a corporation is that an LLC is owned by one or more individuals, and a corporation is owned by its shareholders.

No matter which entity you choose, both entities offer big benefits to your business. Incorporating a business allows you to establish credibility and professionalism. It also provides limited liability protection.

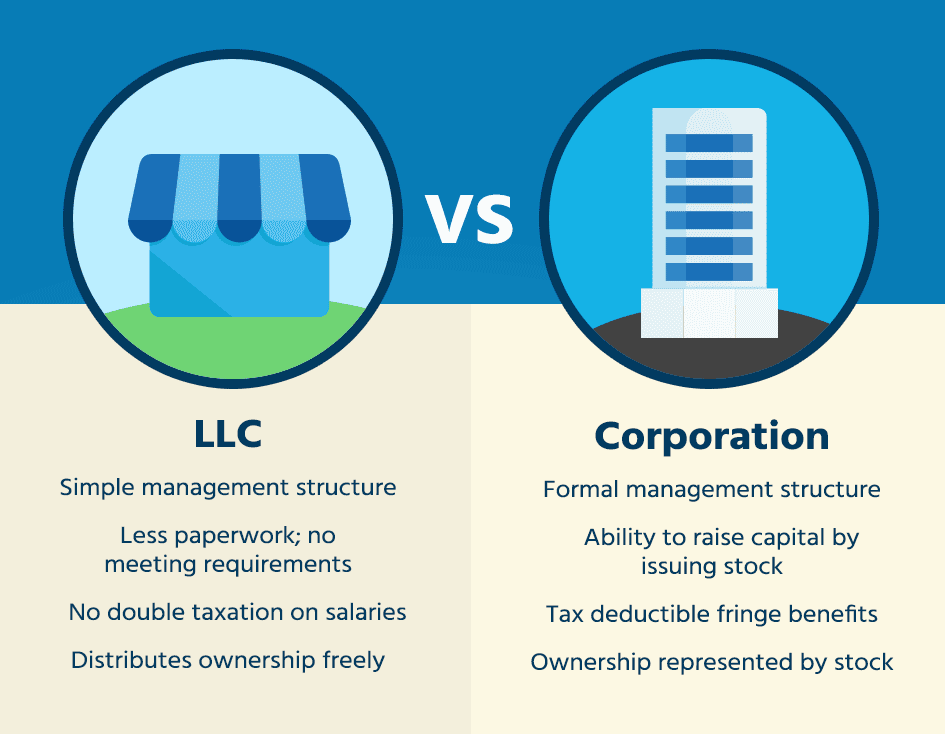

Quick Comparison - LLC vs corporation vs S Corporation

View our chart to see the basic differences between a limited liability company and a corporation:

| Entity Type | Liability | Taxation | Maintenance |

|---|---|---|---|

| Limited Liability Company | Combines limited liability protection with a pass-through tax structure. | IRS rules allow LLCs to choose between being taxed as partnership or corporation. | The easiest entity to maintain with the least amount of formal annual requirements. |

| Corporation | Owners / shareholders have limited personal liability for business related debts. | Separate taxable entity, corporate profits among owners and corporation. | Meetings are required to maintain corporate status. Stock may be sold to raise capital. |

| Non-Profit Corporation | A corporation formed for a charitable, educational, religious, literary, or scientific purpose. | Contributions to charitable corporation are tax deductible. Can get tax exempt status with the IRS. | Annual reports, minutes, meetings are required to maintain nonprofit / tax exempt status. |

| S Corporation | An S Corporation is a tax status, so any existing liability protections from your base entity carry over. | More expensive to create than partnership or sole proprietorship, but offers potential tax savings. | More formality requirements than for a limited liability company which offers similar advantages. |

What Is Limited Liability?

Limited liability is a type of protection for your personal assets. It ensures that your personal liability for the business' debts and obligations is no more than the amount of money you invested in the business. This protects your home, automobiles, and other personal assets from being used to pay off any debts accrued by your business.

Without limited liability protection, your home could be used as collateral to repay the businesses debt after a lawsuit or bankruptcy. This is, by far, one of the greatest advantages gained by forming a business entity.

Now that we have explored what both entity types have in common, let's dive deeper into what makes them different.

Watch our video on LLC vs Corporation to learn more.

Should I Convert My LLC to a Corporation?

Converting an LLC to a corporation can offer advantages, especially for those looking to attract investors or expand the business significantly. Corporations are structured to make it easier to raise capital through stock sales, a key advantage for businesses with plans to grow quickly or bring on additional owners. Corporations also offer a more formal structure with clearly defined roles, which some industries and investors prefer. However, converting to a corporation introduces additional regulatory requirements and potential double taxation, so it's important to consider if these align with the company's goals before making the change.

Which Is Better for Small Businesses: LLC or Corporation?

Choosing between an LLC and a corporation depends largely on the goals and needs of the business. LLCs are generally easier to set up and maintain, making them an ideal choice for small businesses that want flexibility and lower compliance costs. LLCs also avoid the double taxation faced by C corporations, which can help owners maximize their profits. On the other hand, corporations may be a better fit for small businesses planning to grow significantly or seek outside investors. Ultimately, understanding the level of structure needed, tax implications, and growth goals will help determine the best fit.

Is an LLC the same as a corporation?

An LLC is not a type of corporation. In fact, an LLC is a unique hybrid entity that combines the simplicity of a sole proprietorship with the liability protections offered by starting a corporation.

Is It Better to Have an LLC or a Corporation?

From liability protection to tax savings, the benefits of incorporating your business are undeniable. To choose the entity that best fits your business, you need to consider the main differences between the two entities, including taxation, management, annual maintenance requirements, and differences in ownership.

LLC vs Corporation: Tax Differences

One of the biggest differences between corporations and LLCs is the way they are taxed. Let's examine how taxation for each business structure works.

LLC Taxes

An LLC is taxed as a pass-through entity by default. This means that the profits of the business are "passed through" to the owners (called members). Profits and losses are reported on the individual tax returns for the owners, and not at the business level. As a result, filing taxes is often simpler for owners of an LLC. Any losses or operating costs of the business can be deducted on personal tax returns, which can help offset other income.

The rate at which an LLC is taxed depends on the total income of the owner, as it does when you file as a sole proprietor. Owners of an LLC may also be required to pay self-employment taxes. Some states require LLCs to pay a franchise tax. This is a tax issued by the state for the privilege of doing business in that state. Franchise taxes are usually paid annually and vary from state to state.

What happens if you do not pay your taxes? Failing to pay on time or at all could result in penalties and even the involuntary dissolution of your business.

Luckily, incorporating as an LLC provides entrepreneurs with flexibility. An LLC may elect to be taxed as Corporation or an C Corporation. While it is an uncommon choice, filing an LLC as a C Corp tax designation does make financial sense for some businesses.

Corporation Taxes

Corporations are taxed as a separate legal entity, which can earn its own income. Corporations are responsible for paying tax on their profits, (corporate tax), and tax on dividends the entity distributes to its shareholders. Since dividends are not tax deductible (like salaries and bonuses), dividends are taxed twice. This is referred to as double taxation. This is not an issue for smaller corporations where only the owners work for the corporation. Instead, owners receive tax deductible salaries and bonuses.

While double taxation is seen as a disadvantage for businesses choosing to file as a corporation, this additional tax responsibility can often be offset by federal deductions that are only available to corporations.

For example, a corporation may deduct all its business expenses. These can include advertising costs and operating expenses as well as certain employee fringe benefits such as medical and retirement plans. These deductions all add up to substantial savings over time for the business.

As of 2018, corporations pay a flat tax of 21% on their profits, which is lower than the top five individual tax rates. While this is largely offset by double taxation, any income the corporation chooses to retain at the end of the year will be taxed only once at the new 21% rate. This allows the owners of the corporation to save on taxes by investing some profits back into the business.

Keep in mind if a corporation has fewer than 100 shareholders, it can file an S Corporation election. This is a tax status that allows a business to be treated as a pass-through entity much like an LLC. This may be a good option for businesses who want to be taxed like an LLC, but also want some of the additional formalities a corporation provides. The S Corporation designation does allow flow-through taxation (no corporate tax), but there are certain requirements to qualify as an S Corp that may limit its utility to a business.

S Corporation Taxes

If a business qualifies as an S Corporation, the tax difference between an LLC and S Corp is a bit more nuanced. Both an LLC and an S Corp has flow-through taxation (no double taxation). Keep in mind that an LLC's distribution of profits are subject to an employment tax, whereas an S Corp's dividends are not.

For more information about how an S Corporation filing might help you save each year on taxes, check out our S Corporation Tax Calculator.

With careful planning, a small business can avoid significant employment taxes by electing to become an S Corp. However, there can be drawbacks of an S Corp that may deter a small business from taking this advantage. Always consult a professional before deciding on whether to be taxed as an LLC or S Corporation.

You can learn more about the differences between corporation and LLC taxes here in our learning center.

LLC vs. Corporation: Business Ownership

Ownership is another important aspect to keep in consideration when deciding between whether to form an LLC and a corporation. The structure of ownership in each entity is very different, and each has a clear purpose which makes choosing the right entity for your business a bit easier.

When Should You Choose a C Corp?

A C Corporation is ideal for businesses looking to raise significant capital or go public, as it allows for unlimited shareholders and easier access to investors.

A corporation can issue shares of stock and sell percentages of the business to its owners, which are called shareholders. These shareholders can transfer shares, purchasing more stock to own a larger percentage of the company, or selling off stock to own less. If your business is one that wants to attract outside investors, a corporation may be the best entity for it. A corporation also exists in perpetuity separate from the owners, meaning that a corporation remains in existence even when an owner leaves or divests from the company.

When Should You Choose an S Corp?

An S Corporation is a good choice for small to medium-sized businesses that want to avoid double taxation while still enjoying some of the advantages of a corporation. S Corps offer limited liability protection, but income and losses pass through to the shareholders, meaning taxes are only paid at the individual level. This structure is ideal for business owners who want to simplify taxes while maintaining the corporate structure's legal benefits.

When Should You Choose an LLC?

An LLC is a great option for businesses seeking flexibility in management and fewer formalities than a corporation. It's also beneficial for owners who want to limit personal liability while keeping taxes simple, as income passes through to the members and is reported on individual tax returns. LLCs work well for small businesses, startups, and sole proprietors who prefer straightforward taxation and operational freedom without the complexities of corporate governance.

A Limited Liability Company (LLC) has the freedom to distribute its ownership stake to its members without regard to a member's financial contribution to the LLC. Let's use the example where a member of the LLC may not have invested as much capital as another member. An LLC's operating agreement could specify that all members receive an equal share of the profits anyway. This creates additional flexibility when establishing the ownership of the business.

An LLC can also be owned by foreign individuals, other corporations, or any kind of trust. This may make it the right choice for businesses in certain circumstances where these factors are important.

An LLC's operating agreement also outlines the details about how membership interest can be transferred between its members, if at all, and what happens when a member leaves the LLC. By default, if not defined in the operating agreement, when a member leaves the LLC it must be dissolved.

LLC vs. Corporation: Management

An LLC has a flexible management structure. The entity can be managed by its members or a group of managers, and any member may act as the LLC's manager. The LLC may also elect to have no distinction between an owner and a manager of the business. Due to its flexible nature, LLC management is less formal which may make it an ideal entity for some entrepreneurs.

What is the difference between "manager-managed" and "member-managed" LLCs? In a member-managed LLC, the owners themselves oversee running the day to day operations, while a manager-managed LLC generally has investors that sit on the side lines, and don't have any other active role in the business.

A corporation's management structure is much stricter. A corporation must have a formal structure with a Board of Directors handling the management responsibilities of generating profits for the shareholders. Corporate officers are assigned to handle the day-to-day operations of the business. The shareholders are considered owners of the corporation but remain separate from business decisions and daily operations of the corporation (except for approval of major corporate decisions).

However, shareholders retain the power to elect directors, and individual shareholders can be elected as a director or appointed as an officer. The individual rules of any corporation are dictated by its corporate bylaws, which is a detailed set of rules adopted by the Board of Directors after the corporation is formed.

LLC vs. Corporation: Formal Requirements

Both corporations and LLCs are required to fulfill maintenance and/or reporting requirements set by the state where their entity has been formed. This keeps the business in good standing and maintains the limited liability protection acquired by incorporation. While every state has its own rules and regulations that govern both corporations and LLCs, corporations generally have more annual requirements than LLCs.

Corporations are required to hold an annual shareholder meeting each year. These details are documented, along with any discussions, as notes called corporate minutes. A corporation is generally required to file an annual report, too. This helps keep the business' information current with the Secretary of State. Any actions or changes in the business will require a corporate resolution to be voted on at a meeting with the board of directors.

LLCs, on the other hand, have fewer record keeping requirements than their corporation counterparts. For example, an LLC is not required to keep minutes, hold annual meetings, or have a board of directors. While some states still require LLCs to file annual reports, others do not. Check in with your local Secretary of State to determine which requirements are applicable to your LLC entity.

What Is the Difference Between a Legal Entity and a Tax Entity?

Many new business owners get confused when it comes to understanding the difference between legal entities and tax entities. Let's take a moment to unpack their differences.

A tax entity is how the IRS sees your business. Subsequently, this reflects how your business will be taxed. Tax entity examples include C Corporations, S Corporations, and sole proprietorships. Legal entities have a choice about what tax entity they want to identify as. Both an LLC and a corporation can file an S Corp election and choose to be taxed as an S Corporation, even though they are still two different legal entities.

Overall, LLCs have more options when it comes to choosing a tax identity than corporations. However, both legal and tax entities offer benefits that are best consulted with a CPA or attorney that understands the ins and outs of your business.

LLC vs Corporation: Legal Discrepancies

Both LLCs and corporations provide benefits to its owners when it comes to legal protections, although there are differences between the two and how they are seen by the court system.

Corporations have been in existence since the start of U.S. history. Because of this, a corporation as an entity has matured and developed to the point where the laws have become uniform. United States courts have centuries of law history cases to help resolve disputes and issues related to corporations. This creates significant legal stability for corporations.

Limited Liability Companies are still considered to be relatively "new." Their entity was first recognized in the 1970s as the offspring of both the corporate and sole proprietorship/partnership form. Due to this dual nature, an LLC takes on the characteristics of both legal entities. However, as a result of being a "new" legal entity and having characteristics of both a corporation and partnership, states differ in their treatment of LLCs.

While most states have similar LLC laws, there are differences that may lead a business to choose to become an LLC in one state and a corporation in another. In time, LLC laws will become more uniform throughout the United States. For most businesses, these discrepancies between LLC laws should not be a factor, but the discrepancies may be the deciding factor for a few.

LLC vs Corporation: Pros and Cons

When deciding whether to form an LLC or corporation, it's important to consider the unique benefits and drawbacks of each. The choice between an LLC or corporation can impact taxes, legal liabilities, and operational flexibility, so it's essential to weigh the pros and cons carefully.

Pros

LLCs offer greater flexibility in management and fewer formalities compared to corporations. Corporations, on the other hand, provide stronger access to capital and may be better suited for businesses planning to go public or seek outside investment.

Cons

LLCs can be limited in terms of fundraising options, as they typically cannot issue stock. Corporations, meanwhile, face stricter regulatory requirements and more complex tax structures, which can increase operational costs and responsibilities.

How to Choose Between an LLC and Corporation

When deciding between an LLC vs corporation, it's important to consider factors like your business goals, tax preferences, and the level of liability protection you need. LLCs offer more flexibility and simpler tax structures, making them ideal for small businesses. Corporations, on the other hand, are better suited for businesses planning to raise capital, go public, or attract investors. Your decision should align with your long-term business strategy and the level of operational complexity you're willing to manage.

In Summary

Both corporations and limited liability companies, with each entity offering its own benefits, separate the owners from the business and provide limited liability protection for their assets.

Inc vs LLC: How will you know which entity to incorporate a business as? Ultimately, deciding which entity aligns the most with your goals is an important first step to take on the way to forming your business.